PChome Online (8044 TT): Turnaround Signals Emerging; Ecosystem Value Yet to Be Reassessed

Company Overview

PChome Online is one of Taiwan’s leading e-commerce and digital consumer platforms, with businesses spanning B2C e-commerce, marketplace operations, FinTech, logistics, and retail media. Its flagship PChome 24h Shopping has a long-standing position in Taiwan’s 3C category, supported by supplier relationships and fulfillment capabilities. Through 21st FinTech, the group has expanded into BNPL, payment gateway, Pi Wallet, and merchant services. With Uni-President as a strategic shareholder, PChome is gradually evolving from an online retailer into a broader digital consumer platform integrating e-commerce, FinTech, logistics, and retail ecosystem resources.

Key Points

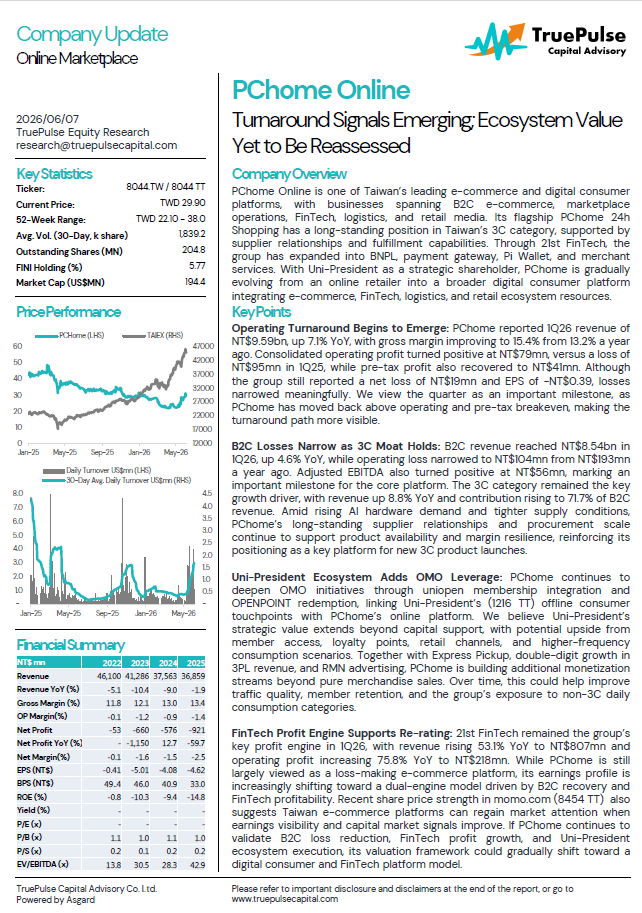

Operating Turnaround Begins to Emerge: PChome reported 1Q26 revenue of NT$9.59bn, up 7.1% YoY, with gross margin improving to 15.4% from 13.2% a year ago. Consolidated operating profit turned positive at NT$79mn, versus a loss of NT$95mn in 1Q25, while pre-tax profit also recovered to NT$41mn. Although the group still reported a net loss of NT$19mn and EPS of -NT$0.39, losses narrowed meaningfully. We view the quarter as an important milestone, as PChome has moved back above operating and pre-tax breakeven, making the turnaround path more visible.

B2C Losses Narrow as 3C Moat Holds: B2C revenue reached NT$8.54bn in 1Q26, up 4.6% YoY, while operating loss narrowed to NT$104mn from NT$193mn a year ago. Adjusted EBITDA also turned positive at NT$56mn, marking an important milestone for the core platform. The 3C category remained the key growth driver, with revenue up 8.8% YoY and contribution rising to 71.7% of B2C revenue. Amid rising AI hardware demand and tighter supply conditions, PChome’s long-standing supplier relationships and procurement scale continue to support product availability and margin resilience, reinforcing its positioning as a key platform for new 3C product launches.

Uni-President Ecosystem Adds OMO Leverage: PChome continues to deepen OMO initiatives through uniopen membership integration and OPENPOINT redemption, linking Uni-President’s (1216 TT) offline consumer touchpoints with PChome’s online platform. We believe Uni-President’s strategic value extends beyond capital support, with potential upside from member access, loyalty points, retail channels, and higher-frequency consumption scenarios. Together with Express Pickup, double-digit growth in 3PL revenue, and RMN advertising, PChome is building additional monetization streams beyond pure merchandise sales. Over time, this could help improve traffic quality, member retention, and the group’s exposure to non-3C daily consumption categories.

FinTech Profit Engine Supports Re-rating: 21st FinTech remained the group’s key profit engine in 1Q26, with revenue rising 53.1% YoY to NT$807mn and operating profit increasing 75.8% YoY to NT$218mn. While PChome is still largely viewed as a loss-making e-commerce platform, its earnings profile is increasingly shifting toward a dual-engine model driven by B2C recovery and FinTech profitability. Recent share price strength in momo.com (8454 TT) also suggests Taiwan e-commerce platforms can regain market attention when earnings visibility and capital market signals improve. If PChome continues to validate B2C loss reduction, FinTech profit growth, and Uni-President ecosystem execution, its valuation framework could gradually shift toward a digital consumer and FinTech platform model.