Grape King Bio (1707 TT): Reshaping Growth Momentum Across Business Segments

Company Overview

Founded in 1969, Grape King Bio (1707.TW) is a leading Taiwan health-supplement company built on vertically integrated fermentation, branded products, and a fast-growing OEM/ODM platform. Its four business units—Taiwan own-brand, OEM/ODM, UVACO, and Shangh1ai—are supported by in-house R&D and decades of fermentation expertise. With a portfolio grounded in functional mushrooms, probiotics, and clinically supported actives, the company serves both domestic consumers and global brands. Backed by a solid balance sheet and steady cash flow, Grape King is focused on product innovation and international expansion to support long-term growth.

Key Points

OEM/ODM as the Primary Execution Platform for Global Expansion: Grape King’s OEM/ODM segment has emerged as the group’s most visible execution platform for global expansion, delivering 54% YoY growth in 2025 on strong customer demand and rising utilization. Expansion into Europe and Japan is accelerating, supported by faster EU ingredient registration and a growing pipeline of patented, clinically validated actives. With increasing traction from international brands and strengthened multi-dosage capabilities, OEM/ODM is forecast to deliver ~29% revenue growth in 2026 and ~35% in 2027. As this platform scales, it extends Grape King’s geographic footprint, enhances earnings visibility, and anchors the group’s medium-term growth trajectory.

UVACO Positioned for Geographic and Category Expansion: UVACO enters the next phase with a stable core in Taiwan and increasing optionality from both geographic expansion and category innovation. The launch of Antrodia Mycelium Beadlets in Nov 2025 reinforces demand for high-value functional products, with momentum carrying into 2026. More structurally, CordiBella marks UVACO’s first expansion beyond supplements into skincare, leveraging proprietary fermentation actives and aligning with a membership base that is over 80% female. This broadens addressable spend and enhances long-term member economics. Looking ahead, the planned Malaysia launch in 3Q26 extends UVACO’s direct-selling model beyond domestic scale limits, adding a new platform for growth and cross-border network expansion.

Taiwan Own-Brand and Shanghai Stabilization: Taiwan own-brand has faced pressure as consumers redirected spending toward overseas travel and as the company cleaned up grey-market channels. With the channel reset largely complete and new wellness products rolling out, we expect a more stable operating environment from 2026. Shanghai remains soft amid consumer downtrading, though Uni-President collaboration is expanding ComeBest distribution, and a new anhydrous collagen OEM product launching in 2026 will support utilization. Stabilization in these markets provides a firmer earnings base and improves overall visibility into the group’s forward trajectory.

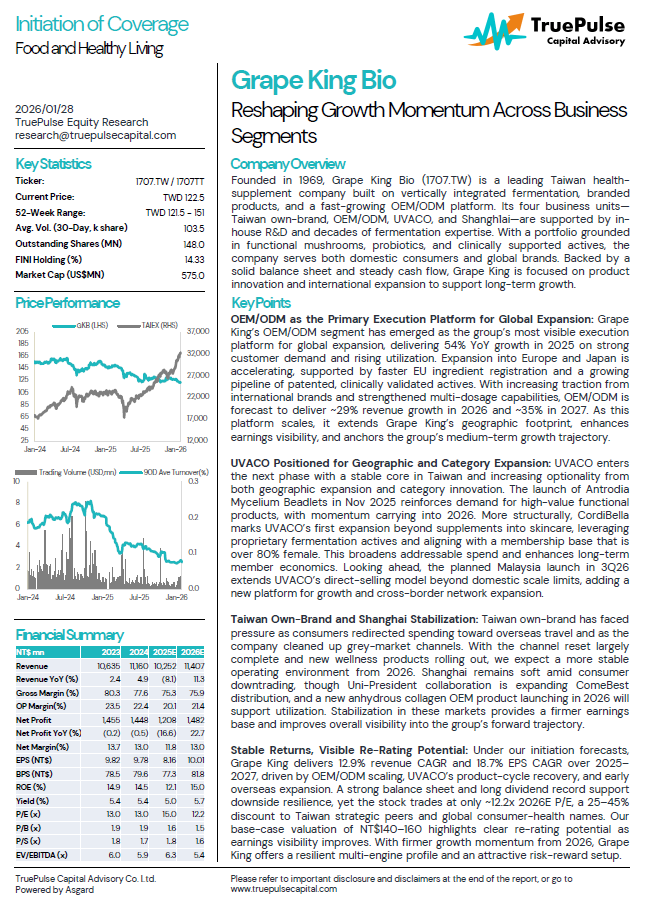

Stable Returns, Visible Re-Rating Potential: Under our initiation forecasts, Grape King delivers 12.9% revenue CAGR and 18.7% EPS CAGR over 2025–2027, driven by OEM/ODM scaling, UVACO’s product-cycle recovery, and early overseas expansion. A strong balance sheet and long dividend record support downside resilience, yet the stock trades at only ~12.2x 2026E P/E, a 25–45% discount to Taiwan strategic peers and global consumer-health names. Our base-case valuation of NT$140–160 highlights clear re-rating potential as earnings visibility improves. With firmer growth momentum from 2026, Grape King offers a resilient multi-engine profile and an attractive risk-reward setup.